Created by Tomáš Dvořák

This is a layout of all that is needed to read about for my Tesla DD.

Tesla's current valuation can be reasonably justified solely on the basis of selling EVs, as their forward P/EBIT of <5 years is <10. (excluding all other present or future revenue streams)

Estimate time needed for Tesla to reach P/EBIT of 10 at current valuation based on their past performance of making and selling EV's.

No clue lol

Confirm or deny consultant dudess' claims about Tesla earnings being inflated by software sales/bitcoin purchases

Do a small qualitative study on why would Tesla possibly want to hide it's production numbers per model (out of all things) and how would it benefit them.

Maybe ask tam ta borka z Deloitte

Is the market share needed for this realistically attainable without a major drop in price and therefore operating margins?

Compare required market share to similar fast-growing "reinvent the wheel" kind-of companies in other industries (mobile phone, pc market), kind of calls for qualitative approach rather than quantitative

Likelyhood of Tesla getting screwed by a random breaktrough in battery production before reaching PE of 10 at current valuation.

Interview battery tech experts at my faculty (or anywhere else)

Calculate most likely EV production capacity growth based on past results.

Test all possible bottlenecks that could limit production capacity (battery supply, chip supply, funding supply)

What drives the disparity between production and deliveries? Is it just lag or something else? Can it be used to improve the precision of the Production & transport cost model?

How well can Tesla's suppliers keep up with their growth, how well they can react to Tesla's expansion? (Based on past results for suppliers to expansion of individual factories) How big of an investment is needed from suppliers to keep up with Tesla, is such investment attainable? Tesla's own battery production excluded as it's a complete dumbster fire rn.

How consistent is Tesla's production and transport cost decrease with Elon's claims about economies of scale (plot PC as a function of time and PC/production_capacity as a function of time, fit exponential function)

Do a qualitative analysis (youtube binge seesion) on what the chip shortage is and how hard it screws Tesla compared to other car manufacturers

Calculation performed in Python

???????

Just fucking guess it I guess

Useful literature/sources:

Does Tesla have enough materials to make their own batteries?

Qualitative analysis

production_cost = revenue*(1-gross_margin)

staff_logistics_cost = revenue*(1-operating_margin+gross_margin)

Calculate operating margin per model:

gross_profit= sum over all models(cost_of_model*units_sold*model_gross_margin)

revenue*operating_margin = sum over all models(cost_of_model*units_sold*model_operating_margin)

(Find best fit, suppose model_gorss_margin and model_operating_margin are exponential functions of time)

Acquire confirmation bias

Dive into Tesla's debt and estimate how sustainable funding growth is this way. How fast can a giga factory pay for itself? How fast can Tesla fund production growth solely from revenues (excluding debt). Calculate production_capacity as function of revenue.

How consistent is Tesla's production capacity growth with Elon's claims of "exponential growth"?

How is does production capacity grow in individual factories?

Explore overall production capacity as a function of assets.

How likely is Tesla to get mode funding? How much more can they go into debt before their balance sheet starts looking sussy wussy?

[I don't even know where to start here. Completely new to corporate loans. Would really appretiate a push in the right direction on where to read up on this]

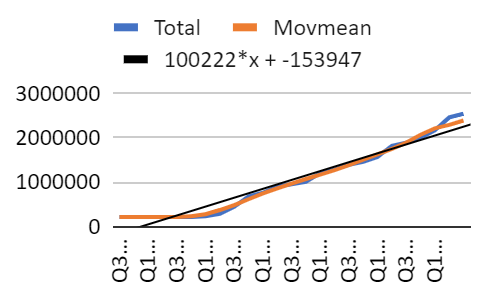

Real production actually quite exponential with time:

(5 year moving mean R^2 >0.99 with exp. fit)

production proportional to e^0.484t (years)

=> YOY production growth of 62%

so far outperforming predicted growth of 50%

Maximum production capacity in individual factories grows in S-curves, which add up to:

Production to assets almost perfectly exponential (R^2=0.95)

production proportional to e^4.72*10^(-2)B USD of assets

=> Increases by 5% for every $1B of assets